Spring is here, which means, depending on where you live, you might be swapping out your heavy winter coat for a jacket that hasn’t seen the outside of your closet since fall.

Reach into those pockets and there is no telling what you will find. A hard candy? A $20 meant for a valet? That receipt your tax accountant’s been badgering you about for 6 months?

A jacket-pocket windfall is nice—and lucky. But it is not the sort of thing you would plan on in your budget.

That is because your budget is too important to leave up to luck.

Don’t Leave Your Exit Up to Luck

In this season of luck—St. Patrick’s Day—celebrating the daily lucky breaks you encounter can be tempting. However, there is a whole genre of quotes from famous people that call luck what it really is: the result of planning and hard work. “Luck is the residue of design”: that’s Dodgers great Branch Rickey. Ray Kroc, the founder of McDonald’s: “Luck is a dividend of sweat.” And Emerson: “Shallow men believe in luck. Strong men believe in cause and effect.”

So why do business owners so often leave an exit up to luck?

Maybe it is a little bit of self-sabotage—planning an exit means you might have to envision a life without your business. While owners are good at the one thing that made their business successful, they may not be good at what might make their business significant.

No matter why an owner is reluctant to prepare for an exit, leaving 80-90% of your wealth up to chance is enough to make even the calmest person a little green around the gills.

Consider another shade of green instead. In Celtic lore, four-leaf clovers protect you from evil spirits and keep bad luck at bay. As business advisors, we know that planning is the only thing that repels bad luck.

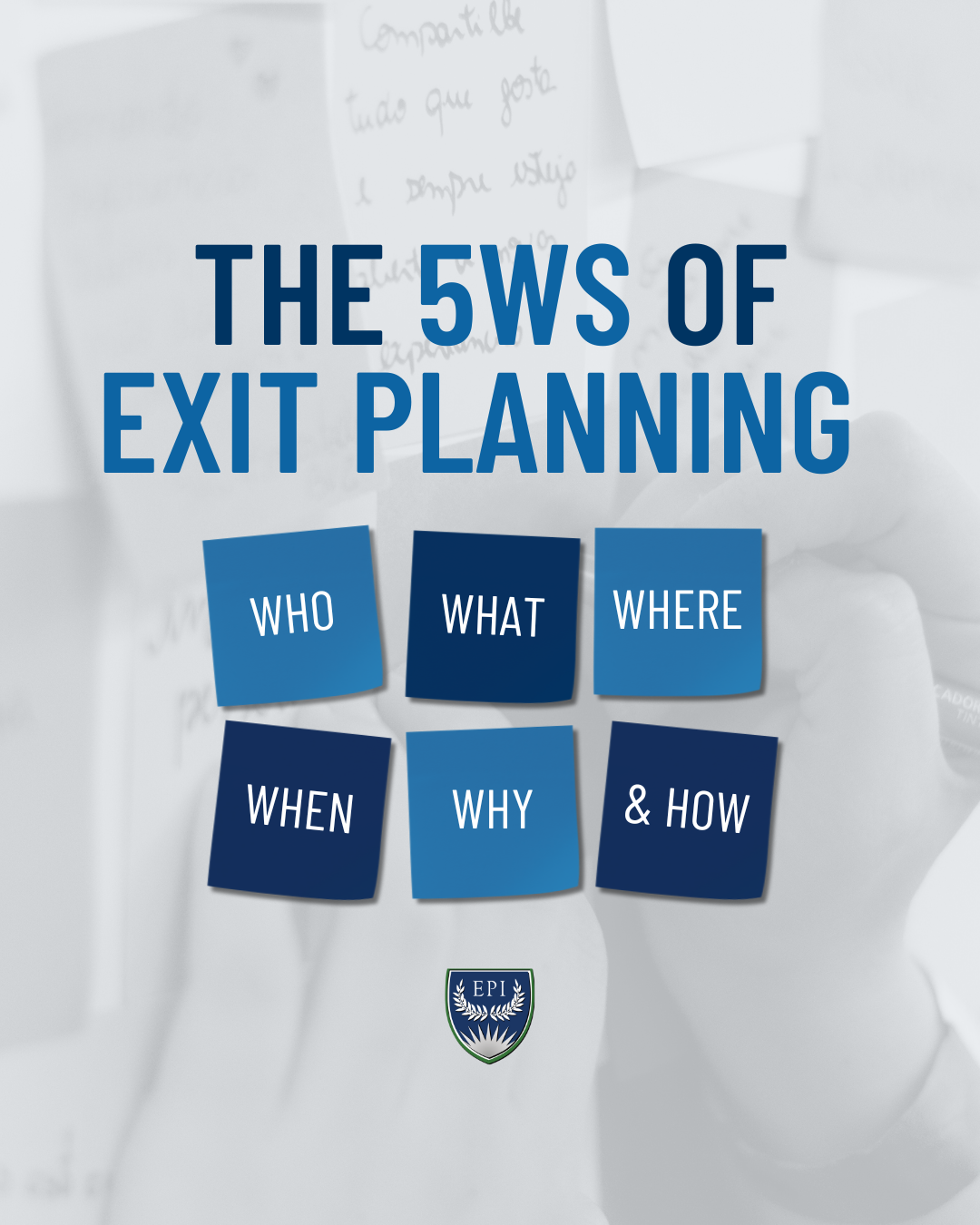

The Four-Leaf Clover of Strategic Exit Planning

Here are four key things to keep in mind to accelerate value:

- Team: Business owners should surround themselves with an external advisory team. Unlike the business’s leadership team, an advisory group should include an attorney, a certified public accountant, a growth advisor or coach, and a financial planner. One of the four should be a Certified Exit Planning Advisor (CEPA®), and they need to operate cohesively to help the owner prepare for an exit on their terms.

- Three Legs of the Stool™ Approach: That team is not just focused on the business, and they are not serving the business necessarily. They serve the owner’s interests first and foremost. In addition to building value in the business, your exit planning team is focused on building personal and financial plans to help the owner thrive post-exit.

- Capitals: Still, much of strategic exit planning is about improving the attractiveness of a business to a potential owner. That means intense focus on the four capitals of every business: human, customer, structural, and social.

- Sprints: It can be daunting when you begin with the end in mind—a successful exit. Instead, plan out 90-day sprints to improve smaller facets of the business that, together, lead to overall value acceleration.

As you work with clients to prepare them for a post-exit life, remember the only luck of the draw they can count on is a highly equipped team ready to implement Value Acceleration Methodology™ practices into play.

Related Resources: